DRAM and NAND costs surged as manufacturers focus on AI HBM, driving cloud price increases; strategies to lock pricing, right‑size resources, and cut costs.

RAM and SSD prices are soaring in 2026, and it’s reshaping cloud services. Here’s why:

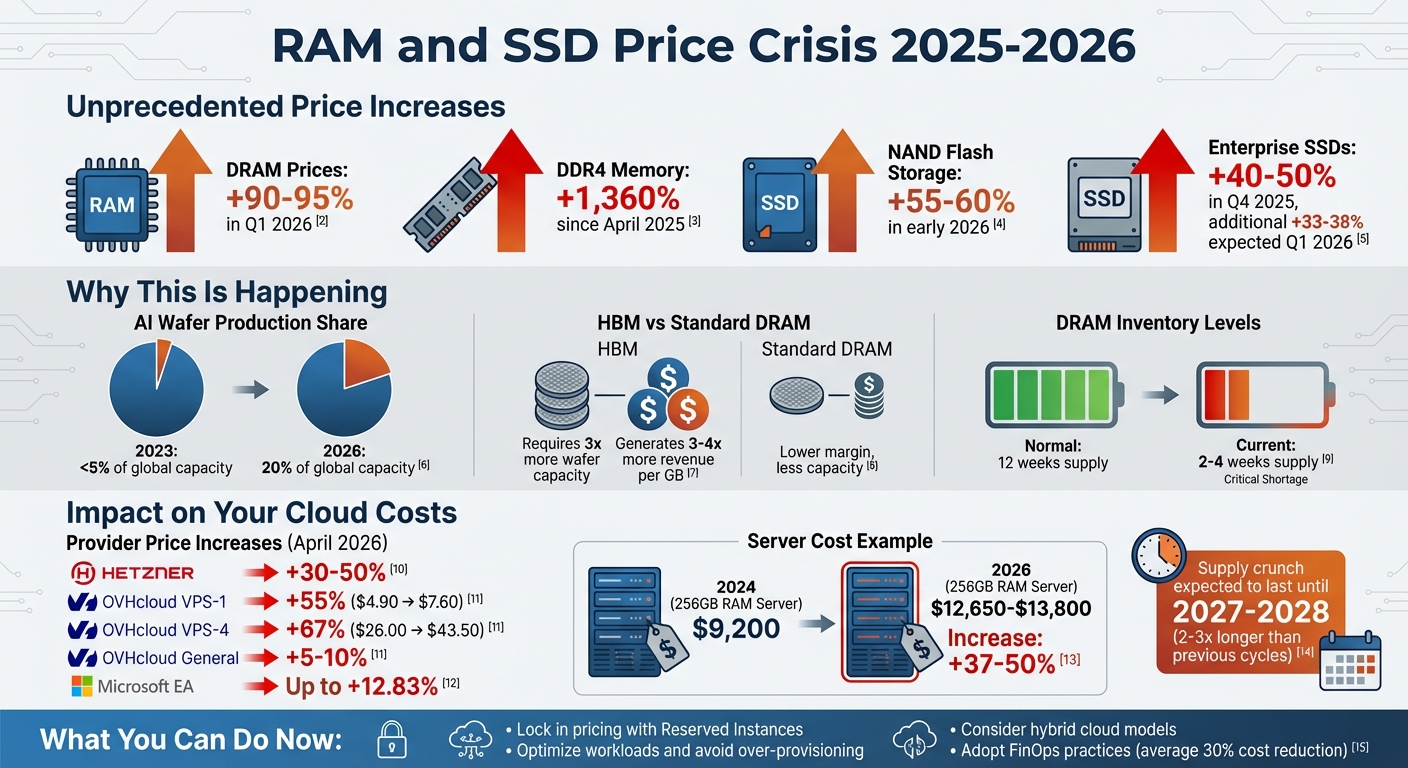

DRAM prices have increased by 90%-95% in Q1 2026, with DDR4 memory spiking 1,360% since April 2025.

NAND flash storage costs jumped 55%-60% in early 2026.

Manufacturers are prioritizing High Bandwidth Memory (HBM) for AI GPUs, which consumes 3x more wafer capacity, leaving less for standard server memory.

AI demand now takes up 20% of global wafer production, up from less than 5% in 2023, creating severe shortages for traditional hardware.

Impact on cloud services:

Providers like Hetzner and OVHcloud have already announced price hikes of 30%-50% for April 2026.

Smaller providers, lacking long-term vendor agreements, are hit hardest, passing costs directly to customers.

What you can do:

Lock in pricing with Reserved Instances or Savings Plans now.

Optimize workloads by avoiding over-provisioning and separating high-performance and archival storage.

Consider hybrid models to balance costs between cloud services and older hardware.

Rising hardware costs are unavoidable, but smart planning can help you manage the impact.

RAM and SSD Price Increases 2025-2026: Impact on Cloud Services

What Is Happening in the DRAM and NAND Markets?

Reduced Production by Key Manufacturers

Key players in the memory industry – Samsung, SK Hynix, and Micron – are shifting their manufacturing focus. Instead of standard server RAM, these companies are prioritizing High Bandwidth Memory (HBM), which is crucial for AI GPUs like NVIDIA‘s H100 and H200. Producing HBM is far more complex than standard DDR memory, involving techniques like stacking multiple dies and using through-silicon vias. This process not only results in lower yields but also requires three times more wafer production capacity compared to DDR5 [2][3].

Building new semiconductor facilities isn’t a quick fix, as it can take three to four years to complete. As a result, manufacturers are reallocating existing production lines, creating a "crowding out" effect. Every wafer used for HBM production reduces the capacity available for standard server memory, which is heavily relied upon by cloud providers [11][2].

The financial appeal of HBM is undeniable – it generates three to four times more revenue per gigabyte than DDR5 [2]. At the same time, older technologies like 2D single-level cell (SLC) flash and earlier generations of 3D NAND are being phased out [10]. This has left infrastructure providers scrambling for components that were once readily available.

By late 2025, global DRAM inventory levels had plummeted from a comfortable 12-week supply to a precarious 2 to 4 weeks[11]. Silvio Muschter, CTO of Swissbit AG, summed up the situation starkly:

RAM becomes four times more expensive because memory is being bought that hasn’t even been produced yet – for GPUs that don’t exist, for data centers that haven’t been built, to serve demand that may never materialize [10]

This production shift is happening just as AI-driven demand is surging, further compounding supply pressures.

AI and Hyperscaler Demand

The reallocation of manufacturing capacity has coincided with a surge in AI-related demand, intensifying the strain on memory supply. In 2023, AI accounted for less than 5% of global wafer production capacity. By 2026, this is expected to rise to 20%[2].

Major cloud providers like AWS, Google, Microsoft, and Meta have locked in HBM supplies through multi-year contracts directly with manufacturers. This leaves smaller players and the broader market in a tough spot, often facing shortages and "allocation" status. In these cases, even paying a premium doesn’t guarantee access to supply [2][10].

The demand isn’t limited to training workloads. As AI expands into inference, the need for high-performance SSDs and LPDDR5x memory is growing to support "key-value cache" storage requirements [6]. This dual demand for both DRAM and NAND has created what Marko Markov of NovoServe describes as a "monopoly game of resources":

AI infrastructure is effectively ‘crowding out’ resources for traditional hosting [11]

Micron disclosed in late 2025 that it could only fulfill 50% to 66% of orders from its primary customers [8]. While the company announced a $24 billion investment in a new NAND memory chip facility in Singapore in early 2026, this additional capacity won’t be operational for several years [1].

The growing demand for AI, coupled with limited supply, has set the stage for volatile pricing and extended shortages.

Price Cycles and Supply Chain Issues

The memory market is now grappling with prolonged pricing cycles and supply chain challenges, driven by the shift in production priorities and surging AI demand. While memory markets have always been cyclical, the current situation stands out. Past cycles – like those in 1993 (spurred by Windows adoption) and 2010 (fueled by smartphones and early cloud computing) – were resolved within 18 to 24 months as manufacturers quickly expanded capacity. However, the current cycle is projected to last until 2027 or 2028, making it two to three times longer than earlier supercycles [2].

The slowdown in DRAM density improvements plays a key role. In the 1990s, density increased 100-fold per decade. Today, it only doubles once per decade [2]. This lag makes it impossible for supply to keep pace with the explosive growth in AI demand.

As LCMH Digital Services explains:

This shortage is not a production accident or temporary logistics disruption. It is a structural reallocation of the semiconductor industry toward artificial intelligence [2]

The pricing impact has been dramatic. Between September and December 2025, average RAM prices for standard server modules (16GB to 128GB) jumped 63%[5]. Enterprise SSD contract prices rose 40% to 50% in Q4 2025, with an additional 33% to 38% increase expected in Q1 2026 [11]. NAND flash prices alone surged more than 60% in November 2025 [8].

For many memory segments, effective capacity for 2026 is essentially sold out. Even with premium offers, buyers struggle to secure reliable allocations without long-term commitments [10]. Meanwhile, server delivery times have stretched from 2 to 3 weeks to 6 to 8 weeks, as manufacturers prioritize hyperscalers over smaller businesses [2].

How Hardware Costs Affect Cloud Providers

Cost Per GB of RAM and TB of NVMe SSD

The rising costs of memory and storage are hitting cloud providers hard. For example, when DRAM contract prices surged by 90% to 95% in just one quarter (Q1 2026), the financial impact was immediate [2]. A server with 256 GB of RAM, which cost around $9,200 in 2024, now comes in at $12,650 to $13,800 – a 37% to 50% jump per node [2].

The size of the provider plays a big role in how this affects operations. Smaller providers, often operating on tighter margins, feel the pressure more acutely. For them, a 40% hike in component costs often translates directly into higher customer pricing. Storage costs have followed a similar trend, with SSDs and HDDs seeing a 30% to 40% price increase since late 2025 [5].

These cost pressures are forcing providers to rethink how they spread out hardware investments and allocate resources.

Hardware Amortization and Overcommit Ratios

Cloud providers typically spread the cost of server hardware over 3 to 5 years. But when hardware prices spike in the middle of that cycle, they face tough decisions: absorb the extra expense or adjust customer pricing to reflect the new reality.

Overcommit ratios – where providers allocate more virtual resources than they physically have, betting that customers won’t use their full allocation at the same time – also take a hit when hardware costs rise. For example, if a server with 512 GB of physical RAM suddenly costs 40% more, the economics of offering low-cost VPS instances on that server become far less viable. OVHcloud tackled this head-on in early 2026 by increasing its VPS-1 tier pricing from $4.90 to $7.60 – a 55% jump – to offset higher RAM costs [3].

To manage these challenges, some providers keep older, fully depreciated servers running for budget-conscious customers. Meanwhile, premium tiers get the newer, pricier DDR5 and NVMe hardware. OVHcloud, for instance, excluded its older "Eco" ranges (like Kimsufi and So You Start) from price hikes, shielding customers using legacy infrastructure [3].

Smaller Providers vs. Hyperscalers

The impact of rising costs isn’t felt equally across the industry. Hyperscalers like AWS, Microsoft, and Google have a significant advantage: multi-year, direct-to-vendor agreements that secure pricing and ensure a steady supply [4]. During memory shortages, manufacturers prioritize these large contracts, leaving smaller providers – who buy servers on shorter timelines or in smaller quantities – struggling to secure components, even at higher prices [2][10].

This dynamic creates a two-tiered market. As Vlad Galabov, Senior Research Director for Enterprise Infrastructure at Omdia, explains:

The massive hyperscalers (AWS, Microsoft, Google) negotiate long-term, direct-to-vendor agreements that insulate them from these immediate price shocks. However, smaller and mid-sized providers… have no choice but to pass these costs directly to their users [4].

For hyperscalers, a 40% increase in RAM costs might translate to just a 5% to 10% rise in overall data center expenses, thanks to resource pooling and economies of scale [2]. Smaller providers don’t have the same cushion.

Take Hetzner, a German provider, as an example. In February 2026, Hetzner announced price increases of 30% to 50% across its data centers in Germany, Finland, the US, and Singapore, effective April 1, 2026. The company attributed this to "drastic" increases in infrastructure and hardware costs [1][4]. Some server instances saw monthly price hikes exceeding $100. Galabov noted that while a 50% increase may seem steep, it reflects "the brutal reality of the current hardware supply chain" [1][4].

OVHcloud also adjusted its pricing to cope with these pressures. In November 2025, CEO Octave Klaba announced that cloud prices would rise 5% to 10% between April and September 2026, with RAM-heavy configurations seeing the largest increases. For example, the company’s ADV-3 Gen4 bare metal server saw its monthly price rise from $210 to $255 [3]. Klaba elaborated:

At OVHcloud, we estimate that the same server produced in December 2025 and December 2026 will cost between +15 percent and +35 percent more [1].

Smaller providers face additional challenges, like longer lead times for new servers. In 2024, server delivery times for small and medium businesses averaged 2 to 3 weeks. By 2026, those lead times stretched to 6 to 8 weeks, as manufacturers prioritized hyperscale orders [2]. This forces smaller providers to plan further ahead and tie up more capital in inventory, adding yet another layer of complexity.

Will VPS and Cloud Server Prices Increase?

Impact of Hardware Costs on Pricing

The rising costs of hardware components are already driving price hikes, with this trend expected to continue through 2026. For example, DRAM prices have surged by 90% to 95% in just a single quarter, while NAND flash prices have risen by 55% to 60%. These increases directly affect providers, especially smaller and mid-sized ones that lack the purchasing power of hyperscalers. With tight operating margins, these providers are left with little choice but to pass on the added costs to their customers.

Configurations requiring large amounts of RAM have been hit particularly hard, as have storage-heavy workloads reliant on SSDs. The significant uptick in hardware costs makes it challenging for providers to absorb these expenses without adjusting their pricing models. Recent announcements from major providers confirm this trend, illustrating how these cost pressures are reshaping the market.

Verified Pricing Adjustments

Several well-known providers have already raised their prices in response to these challenges. Hetzner, for instance, announced in February 2026 that prices across its data centers in Germany, Finland, the US, and Singapore would increase by 30% to 50%, effective April 1, 2026. For some dedicated server plans, this means monthly costs have jumped by over $100 due to rising hardware and operational expenses [1][4].

OVHcloud took a more selective approach, with CEO Octave Klaba confirming price hikes of 5% to 10% across various services between April and September 2026. Specific examples include the VPS-1 plan, which increased from $4.90 to $7.60 (a 55% jump), and the VPS-4 plan, which rose from $26.00 to $43.50 – a 67% hike. These changes are largely attributed to the rising costs of RAM and high-density NVMe storage [3][7].

Even hyperscalers are not immune to these trends. On November 1, 2025, Microsoft removed volume-based discounts for Enterprise Agreement customers, leading to cost increases of up to 12.83% for the largest enterprises. For a hypothetical $30 million contract, this translates to an additional $3.85 million annually [7]. These examples highlight how component cost increases are impacting pricing across the board.

Market Trends and Outlook

The current price hikes are part of a larger, structural shift in the market. Reduced production capacity and the growing demand for AI hardware are reshaping the industry. Manufacturers are prioritizing AI components like High Bandwidth Memory (HBM) for GPUs, which now require three times the wafer capacity of standard DRAM. This shift has created a severe shortage of traditional server memory, the likes of which hasn’t been seen in decades [2][7].

While new fabrication plants are in the works, they won’t be operational until 2027 or 2028, meaning the supply crunch could last another 18 to 24 months. OVHcloud has projected that a server built in December 2026 will cost 15% to 35% more than one made in December 2025 [1]. While hyperscalers benefit from long-term agreements that delay immediate price changes, smaller providers are feeling the impact much sooner. For businesses relying on cloud infrastructure, the real question isn’t whether prices will rise, but when – and by how much.

What This Means for Cloud Desktops and VDI Providers

RAM-Heavy Workloads and Persistent Storage Needs

The recent shifts in DRAM and NAND markets have created serious pricing challenges for cloud desktops and VDI providers. Unlike traditional web hosting or application servers that can share resources dynamically, virtual desktops require dedicated memory for each instance to function effectively. This dependency on dedicated RAM becomes a major cost factor when DRAM contract prices surge by 90% to 95% in just one quarter, compounded by enterprise SSD contract prices rising 40% to 50% during the same period [2][6]. These rising costs make multi-tenant desktop hosting significantly more expensive.

Additionally, VDI environments rely on high-performance SSDs to manage user profiles, application data, and session persistence. With SSD prices expected to climb another 33% to 38% in Q1 2026, providers are facing increasing financial pressure on storage as well as memory [1][4]. The growing demand for HBM production to support AI applications only adds to the strain, as it consumes three times more wafer capacity, further limiting the availability of standard server RAM critical for VDI infrastructure. This creates a challenging landscape where customer expectations and volatile costs are in constant conflict.

Pricing Stability vs. Infrastructure Volatility

On top of these hardware cost challenges, providers are now struggling to maintain price stability while dealing with rapidly increasing component costs. Customers expect predictable monthly pricing, but the reality is that hardware costs can spike dramatically in a short period. For example, DDR5 memory kits (64GB) nearly quadrupled in price between September and December 2025, while DDR4 memory saw an astonishing 1,360% price increase between April 2025 and early 2026. These market shifts are structural and cannot simply be offset by operational efficiencies.

The impact of these rising costs varies depending on the provider’s size. Large hyperscalers like AWS, Google, and Microsoft are somewhat shielded from immediate price shocks due to long-term, direct-to-vendor agreements. In contrast, mid-sized and smaller VDI providers lack this purchasing power, forcing them to pass these cost increases directly to their customers. OVHcloud’s CEO, Octave Klaba, highlighted this reality when discussing targeted price increases:

At OVHcloud, we estimate that the same server produced in December 2025 and December 2026 will cost between +15 percent and +35 percent more.

To navigate this volatility, providers often adopt a mixed approach, using fully amortized legacy hardware alongside cutting-edge systems. This creates a two-tiered market where businesses must decide between predictable rates with older hardware or paying a premium for access to newer, high-performance systems. Understanding these shifting dynamics is crucial for businesses planning their investments in cloud desktop infrastructure.

sbb-itb-bea6502

What Businesses Can Do Now

Lock in Predictable Pricing

One of the smartest moves businesses can make right now is to lock in current pricing before the anticipated increases hit between April and September 2026. By purchasing Reserved Instances or Savings Plans, companies can secure rates for one to three years, shielding themselves from the projected 5% to 10% price hikes by providers like OVHcloud [7]. This strategy works best for workloads with steady, predictable resource needs, allowing businesses to commit to specific capacity levels without the risk of over-provisioning.

Another way to protect against market fluctuations is through multi-year contracts with infrastructure providers [2]. Major players like AWS, Google, and Microsoft often negotiate long-term agreements directly with vendors, helping to shield their customers from sudden hardware cost spikes – an advantage smaller providers may not offer [4]. If your provider offers fixed-rate agreements, make sure to negotiate clear terms, including price caps or indexed adjustments, to ensure protection over the contract period [8][9]. By locking in predictable pricing now, businesses can set themselves up for better resource management down the line.

Optimize Provisioning and TCO Analysis

Getting the most out of your infrastructure starts with right-sizing. Instead of defaulting to maximum specifications, analyze actual resource usage data when provisioning new instances [8]. Over-provisioning, especially for memory, can be a costly mistake right now, given the steep rise in DRAM prices, which has made RAM-heavy configurations more expensive than ever [2][3].

Storage is another area ripe for optimization. Separate high-performance datasets that require NVMe drives from backups and archives, which can be stored on more affordable "cold" storage tiers [3]. Enforce strict data retention policies and make sure to disable unused instances [7]. For networking, consider strategies to cut down on egress fees, such as employing CDNs, using data compression, and relying on private IP addresses for internal transfers [7]. With egress fees accounting for 6% to 15% of total cloud storage costs, these steps can lead to noticeable savings [7].

Here’s a real-world example: In February 2026, the French firm LCMH helped a client avoid the high costs of refreshing their 15 on-premise servers, which would have cost €180,000. Instead, the client migrated to AWS, adopting a monthly cloud model at €4,500. This move not only delivered immediate ROI but is also projected to save €18,000 over three years, even factoring in the rising cloud prices [2].

Balance OpEx and CapEx

Balancing operational expenses (OpEx) and capital expenses (CapEx) has become more critical in today’s volatile market. Traditional hardware refresh cycles now come with steep challenges – server costs have surged by 40% to 50%, and delivery lead times have stretched to six to eight weeks [2]. OVHcloud estimates that a server built in December 2026 could cost 15% to 35% more than one manufactured just a year earlier [1].

Cloud models offer a level of predictability that traditional hardware purchases simply can’t match right now. For businesses considering long-term infrastructure costs, comparing fixed monthly cloud pricing to the rising costs of hardware refresh cycles is essential. Even though cloud prices are climbing by 5% to 10%, hyperscalers like AWS benefit from long-term vendor agreements that buffer against sudden price spikes [4][7]. For workloads with consistent demands, a hybrid approach can be effective: shift steady workloads to older, amortized hardware tiers for cost stability, while leveraging the cloud for high-performance or fluctuating needs [3]. This strategy turns unpredictable capital spikes into manageable operating expenses [9].

Adopting FinOps practices can also bridge the gap between finance and engineering teams, fostering shared accountability for cloud spending. On average, this approach leads to a 30% reduction in cloud costs [7]. Staying informed about DRAM and NAND trends through sources like TrendForce and monitoring supplier earnings calls can also help businesses anticipate price shifts and plan accordingly [8]. These proactive steps can help companies navigate the current market challenges while maintaining efficiency.

Cloud desktops are built on RAM and high performance SSD storage, so hardware pricing cycles affect the entire industry. At flexidesktop, our goal is to keep pricing predictable and avoid surprise changes. To do that, we plan capacity ahead and prioritize infrastructure choices that reduce short-term exposure to market volatility.

We also prefer longer-term infrastructure planning where it makes sense, because it helps us forecast costs more reliably and keep service levels consistent. That does not make us immune to market shifts, but it can reduce how abruptly those shifts translate into customer-facing changes.

Industry-Wide Pressure and What It Means for Customers

Across the hosting and cloud market, providers are already adjusting pricing as component costs rise and supply becomes tighter. When RAM and SSD costs move quickly, the most visible impact tends to show up first in RAM-heavy and storage-heavy services, including virtualization and VDI-style workloads.

As of March 2026, flexidesktop pricing has remained unchanged. We understand that predictable monthly costs matter, especially for small businesses planning budgets and comparing cloud subscriptions against traditional hardware refresh cycles. If broader market conditions eventually require a pricing update, we will communicate it clearly and well in advance, so customers can make decisions with enough time and context.

Conclusion

Price fluctuations in the memory and storage markets are nothing new. The current spike in DRAM and NAND costs – fueled by AI demand and a shift toward High Bandwidth Memory – fits a familiar pattern. For instance, DRAM contract prices shot up by 171.8% year-over-year as of Q3 2025, while DDR5 prices skyrocketed by 307% since September 2025. These shifts underline how multi-year production cycles and delays in bringing new fabrication plants online contribute to these price swings [7].

Even with these price hikes, the advantages of cloud services remain undeniable. Cloud infrastructure offers operational flexibility and scaling capabilities that on-premise systems simply can’t match. Plus, hyperscalers often leverage long-term vendor contracts to shield their customers from sudden price shocks. Take the example of a digital services client in Alsace, France: instead of spending $180,000 to upgrade 15 on-premise servers in 2026, the company moved its workload to AWS for $4,500 per month. Over three years, this migration saved them $18,000 [2].

To navigate these market dynamics, businesses should focus on strategic planning. Locking in predictable pricing with Reserved Instances or Savings Plans, optimizing configurations based on actual usage data, and shifting non-critical workloads to older hardware tiers can make a big difference. In fact, companies that adopt FinOps practices report an average 30% reduction in cloud costs [7]. Whether you rely on the cloud or stick with on-premise systems, understanding these pricing trends helps you make smarter decisions about when to invest, how to optimize, and where to strike a balance between capital and operational expenses. While the current price surge will eventually stabilize, businesses that adapt now will position themselves for future success.

Lock in your cloud desktop price before costs rise further

flexidesktop’s Desktop as a Service plans start at $19/month — fixed pricing, no hardware to buy, no RAM shortage to worry about. Try it free.

FAQs

How long will RAM and SSD prices stay high?

Prices for RAM and SSDs are projected to stay high until at least 2026, with the possibility of this trend extending into 2027. The main culprits? Supply shortages and rising demand driven by AI advancements and hyperscaler data centers.

Manufacturers are prioritizing high-margin AI memory production, which has led to a drop in the supply of standard DRAM and NAND flash. As a result, costs for these components have increased. Industry analysts believe these challenges will persist until supply chains regain stability – a process that could take several years.

Which cloud workloads get more expensive first?

Workloads that demand substantial memory and storage – like virtualization, virtual desktop infrastructure (VDI), and data-heavy applications – are usually the first to feel the strain. These workloads depend heavily on DRAM and NAND flash, which makes them particularly vulnerable to rising hardware costs. Smaller providers often experience these challenges earlier since they typically lack robust supply chain flexibility. On the other hand, larger providers can sometimes postpone price hikes by leveraging inventory management strategies.

How can I cut cloud costs without downgrading performance?

To cut cloud costs without compromising performance, start by right-sizing your resources – align them closely with actual workload needs to prevent overprovisioning. Consider locking in predictable pricing through long-term contracts or fixed monthly plans, which can shield you from fluctuations in hardware costs. You can also save by optimizing workload placement, consolidating tasks, and adopting efficient architectures to minimize resource usage while keeping performance steady.

Israel de la Torre is the founder of flexidesktop and has spent 15+ years working in cloud infrastructure and Windows virtualization. He helps businesses migrate from on-premises Windows setups to managed cloud desktops.

Compare remote-access apps and cloud desktops to choose the right RDP alternative—use remote tools for occasional access or cloud PCs for always-on team work.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.